Solvent on paper, short on dollars: the Maldives economy in mid-2026

The IMF saw resilience. Maldivians saw their cards declined.

Artwork: Dosain

22 Jun, 17:30

That is the good news. The bad news is the same news: the black market rate for US dollars hit MVR 20.50, well above the MVR 15.42 peg and the worst since the pandemic. It has now sat above MVR 20 longer than at any time on record. Facing demand it could not meet, the Bank of Maldives capped foreign card spending and limited customers to 30 overseas e-commerce transactions a month. Many Maldivians spent the past three weeks unable to pay for streaming services, app stores and online subscriptions, despite the bank insisting that such payments "do not fall under the daily foreign spend budget."

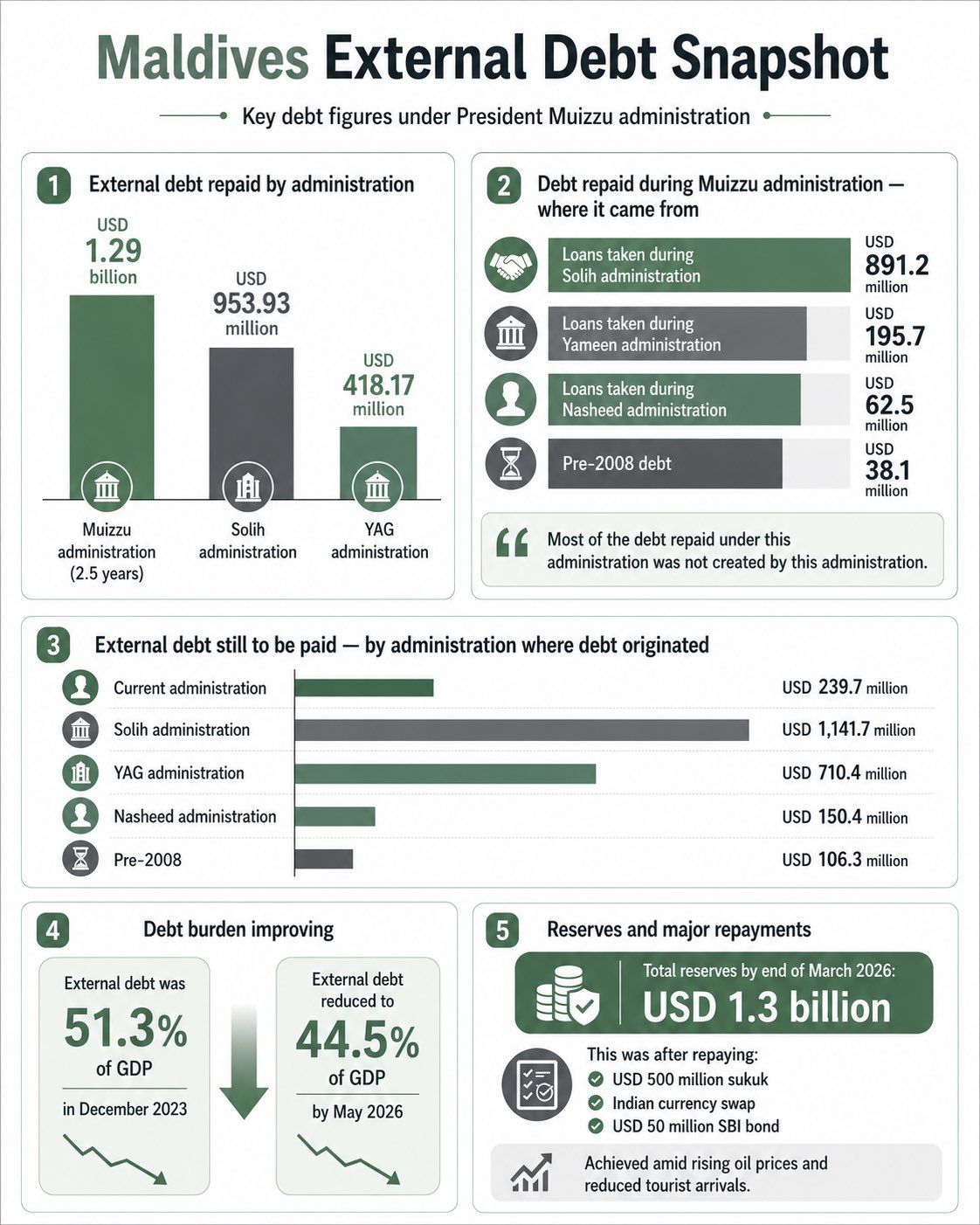

But the government hears only the good news. "President [Dr Mohamed] Muizzu's administration has handled the debt situation of Maldives in a disciplined and responsible manner," ruling party lawmaker Ahmed Azaan wrote on Thursday, alongside an infographic showing the administration repaying US$ 1.29 billion in external debt over two and a half years, bringing it down from 51.3 percent of GDP in December 2023 to 44.5 percent by May 2026.

"These are signs of a government facing a difficult debt situation with seriousness and responsibility."

Most of the debt was borrowed under previous governments, he noted. But critics countered with the Muizzu administration's accumulation of US$ 2.4 billion worth of debt with no major infrastructure development to show for it.

"The Fitch upgrade is welcome news. But avoiding a crisis and solving a crisis are not the same thing. The immediate risk of default has eased following the repayment of the USD 500 million sukuk. That is positive. The Maldives has moved away from the edge of the cliff," former economic minister Ahmed Mohamed wrote on June 5.

But he cautioned that foreign currency reserves cover less than a month of imports and public debt remains well above 100 percent of GDP. The fiscal deficit and current account deficit were projected to reach 14.6 percent and 17.5 percent of GDP respectively.

"The real test is not whether the country avoided default this year. The real test is whether this breathing space is used to put the public finances on a sustainable path," he suggested.

According to finance ministry figures, total state debt reached MVR 155 billion – 130 percent of GDP – by the end of last year, up from MVR 126 billion when the administration took office. A growing share of it is now raised at home. Locked out of affordable external markets by prohibitive rates, the government has leaned heavily on bonds and treasury bills sold domestically, which made up nearly 90 percent of last year's new financing. Much of that domestic debt is itself dollar-denominated.

But across social media, government supporters echoed Azaan, hailing the president's "decisive leadership" and casting the ratings upgrade as a rebuke to doubters at home and abroad. One widely shared post declared the "opposition silenced" and the "foreign rating agencies that assumed the Maldives had collapsed" forced to face reality, predicting that an economy "previously on life support" would now stabilise and win back investor confidence.

However, on Fitch's own scale, the CCC- rating remains a grade reserved for borrowers where default is a real possibility. In the same breath that it commended the authorities for navigating the challenging environment, the IMF also warned that the country's risk of debt distress "remains high."

Nonetheless, Fitch judged that imminent default risk had eased once the sukuk was cleared. Sovereign and guaranteed external debt-service obligations for the second half of the year fall to around US$ 535 million, from US$ 1.1 billion in the first half.

Welcoming the ratings upgrade, the finance ministry touted the sukuk repayment and revenue-side reforms, citing a fall in public and publicly guaranteed debt to 121.2 per cent of GDP by the end of April, below where it stood when the administration took office. Any new borrowing would not undermine debt sustainability, it pledged. The Maldives was now better placed to weather "global headwinds" created by the Middle East conflict than in past cycles, the ministry assured.

Twin deficits

Fitch located the heart of the problem in the country's perennial "wide twin deficits": successive governments spending more than it earns, in a country that imports more than it exports, and plugging both gaps by borrowing.

The World Bank's biannual update released last week projects that growth will collapse to 0.7 percent in 2026, down from an estimated 6.3 percent in 2025, "reflecting significant disruptions to tourism from the conflict in the Middle East due to flight cancellations, compounded by higher fuel prices and tighter financing conditions." The Bank cut the forecast by 3.2 percentage points from its October estimate. The fiscal deficit, which the government narrowed to 4.3 per cent of GDP last year, is forecast to blow back out to 10.9 per cent (less gloomy than the 14.6 percent projected by Fitch) – more than double the government's own 7.1 per cent target – as energy subsidies and a rebound in capital spending collide with weaker tourism revenue.

The current account deficit, squeezed to 7.5 percent of GDP in 2025, is expected to widen sharply again to 20.6 percent on the World Bank's reckoning. Public debt is projected to climb above 140 percent over the medium term. The World Bank's verdict was the same as the IMF's: the Maldives "remains at high risk of debt distress".

The IMF, whose staff closed their annual Article IV consultation visit last week, put 2026 growth at about one percent. The mission credited the authorities with meeting debt obligations on time and called the financial system stable. But it warned that downside risks dominate and singled out the same longstanding recommendations the other institutions did: a systematic review of subsidy schemes with means-testing to protect the vulnerable and tighter control of state-owned enterprises, which it called "a material source of fiscal and governance risk".

The books begin to turn

The finance ministry's weekly fiscal report shows an overall deficit of MVR 110.6 million by June 4, after recording a surplus of just over MVR 1 billion at the same point in 2025. But cumulative tax collections rose to MVR 19.1 billion from MVR 17.3 billion last year, led by business taxes and the tourism goods and services tax.

The deficit reopened because spending outstripped income. Subsidies were the runaway item. By early June, they reached MVR 2.3 billion, up almost 69 percent year-on-year and already about 80 percent of the full-year allocation with nearly seven months left. The public sector wage bill climbed as well by MVR 477.4 million to MVR 5.3 billion, even as the government merged ministries and ordered "right-sizing" of the bloated workforces of several state companies.

The cost of clearing the April debts shows in the same ledger: loan repayments accounted for about a third of all government spending so far this year. By the most recent figures, monthly revenue has begun to fall, down about six percent as tourism tax and fee receipts weaken.

The government narrowed the budget deficit in 2025 mainly by deferring capital spending and bills. The World Bank warned explicitly that unpaid commitments have piled up as arrears across ministries and SOEs.

The same bottleneck

Official reserves, which had recovered to US$ 1.3 billion in March, fell to US$ 718 million by April once the sukuk was settled, enough to cover just 1.4 months of imports. Clearing the sukuk nearly drained the Sovereign Development Fund, which Fitch says fell to about US$ 21 million by the end of April. Usable reserves – the funds readily available after short-term obligations – were at US$ 244 million on Fitch's measure and US$ 148 million on the World Bank's stricter definition. A thin cushion either way.

Public anger has fallen largely on BML, but the transaction limits are only the latest in a year of escalating restrictions the bank has imposed as the dollar shortage has worsened. A 30 percent surcharge slapped on Chinese shopping sites last July almost exactly reflected the black market premium. The measures announced in early May limited customers to 30 overseas e-commerce transactions a month – a threshold BML said fewer than three percent of customers ever reached – to spread scarce dollars more widely. According to CEO Mohamed Shareef, it was intended to curb a minority using personal cards to bulk-buy from sites such as Temu and Shein.

But the wall most customers hit was something the bank had not announced: a separate daily budget applied per website, which returned a terse decline – "Daily budget for this website from local currency cards reached" – with no published limit and no stated reset. Many learnt the rule only when their cards stopped working. The failures were not confined to discretionary spending. Many reported being unable to renew the Adobe and Microsoft subscriptions they need for work or to pay for advertising on Facebook and other platforms.

BML maintains subscriptions were never subject to the limits and has asked customers to report failed payments for individual fixes, an assurance at odds with the steady complaints on its own social media feeds. The bank says the limits will ease before the month is out.

Under rules tightened from June 2025, banks must sell 90 percent of their foreign-currency proceeds to the Maldives Monetary Authority. While reserves duly recovered, the supply that businesses and individuals once drew on shrank and the parallel market worsened rather than disappeared.

Last year, under the mandatory conversion regime, 182 resorts exchanged US$ 671 million, of which the banks passed US$ 523.4 million – about 78 percent – on to the MMA, according to the central bank's annual report. The MMA released US$ 447.6 million back to the banks over the same period for business and public use.

Banks are the bridge between the MMA and the public, one financial sector official told Dhauru, but they can only release what the central bank allows, leaving them unable to meet demand. The MMA has the legal authority to act against the open black market, where authorised exchange agents in Malé and Hulhumalé trade dollars above the peg in plain view, the officials noted.

The dollar shortage is partly seasonal. The May-to-August tourism low season, when resort dollar inflows thin out, coincides with the Hajj and Umrah pilgrimages and school holidays, all of which send Maldivians scrambling for foreign currency at once. This year that familiar squeeze arrived on top of the Iran war, the debt repayments and the dollar conversion rules.

That has prompted bleak forecasts. Former President Abdulla Yameen told a People's National Front gathering on Thursday night that the rate could pass MVR 21 before the end of 2026, challenging government claims that prices would hold. In a country that imports nearly everything, a dollar this strong against the weakened Rufiyaa must feed through to the shelves.

Riyaz Mansoor, a former state minister for economic development, reached the same MVR 21 forecast and offered a pointed explanation for how the rate had stayed so flat until now. From November 2024, when the dollar first touched MVR 20, to May 2026, it barely moved, holding between MVR 20 and MVR 20.20 through a year and a half of Hajjs, Umrahs and school breaks that would normally have pushed it up.

"The cause for this result can only be that the central bank is releasing dollars to maintain the black market price, one way or another. However, with recent loan repayments and dollar outflows, the central bank's ability to maintain its control on the black market is now lost," he wrote on X. The next three months of weak low-season earnings will test how far the rate climbs, he added.

The war, the bills and the cushion

Tourist arrivals are down five percent so far in 2026 after the Middle East conflict shut airspace and cancelled flights from key European source markets. The World Bank estimates the shock has already nudged unemployment up and shaved up to two percent off real wages in the service sector, where informal workers are least protected.

Consumer prices meanwhile rose 4.18 percent in April month-on-month, a sharp increase driven overwhelmingly by a startling 411 percent jump in the unit price of electricity after the unwinding of the tariff discounts for Ramadan.

Inflation bites hardest in the atolls, where prices rose 5.56 percent compared to 3.24 percent in Malé, home to more than nine in 10 of the country's poor. The World Bank estimated that nearly half the population – 48.9 percent – live just above the poverty line, close enough that a 10 percent rise in food prices alone would push the poverty rate up by 1.6 percentage points.

The World Bank projected inflation to rise to six percent this year and to remain above four percent through 2028 "due to intensified foreign exchange (FX) constraints and demand pressures for food and essential goods."

Saruvash Adam, a former finance ministry budget executive, traced the roots of the Maldivian economy's instability to the "twin deficits" when asked recently how the malaise might finally be overcome.

"Both gaps [fiscal deficit and current account deficit] were financed mainly through debt for years. That works for some time, especially in a tourism economy," he explained. "But eventually the imbalances accumulate and begin to pressure reserves, FX liquidity, debt sustainability, and confidence. That is why this is not simply a [temporary] dollar shortage issue. It is a structural imbalance."

The ultimate solution "will not be popular or easy," he warned. The long-overdue adjustment he proposed includes curbing wasteful spending and debt-financed deficits, lifting productivity and domestic production, weaning the country off imports, and earning foreign currency through new channels to rebuild reserves and confidence.

A year ago, the dollar stood at MVR 19.70 and the country was bracing for the repayments to come. The repayments were survived. The dollar is now higher than ever. In Saruvash's view, the state of the economy is the product of "attempts to manage and prolong an unsustainable situation while avoiding the harder economic adjustments."

Discussion

No comments yet. Be the first to share your thoughts!

No comments yet. Be the first to join the conversation!

Join the Conversation

Sign in to share your thoughts under an alias and take part in the discussion. Independent journalism thrives on open, respectful debate — your voice matters.

Support Independent Journalism

Help us keep the news free and fearless

Give once

$

or

Become a memberfrom $5/month