Banks will lower interest rates, says finance minister

Commercial banks in the Maldives have agreed to lower interest rates on loans after the central bank slashed interest rates for the sale of treasury bills (T-bills) with effect from October 28, Finance Minister Abdulla Jihad has said.

02 Nov 2015, 09:00

Commercial banks in the Maldives have agreed to lower interest rates on loans after the central bank slashed interest rates for the sale of treasury bills (T-bills) with effect from October 28, Finance Minister Abdulla Jihad has said.

Speaking at a ceremony held last night to unveil new banknotes, Jihad said one of the reasons for halving interest rates on T-bills was to facilitate lending from banks to the public at lower interest rates.

“We talked to banks before we lowered the rate and got their endorsement. God willing, interest rates on bank loans will be very much lower in the near future,” he said.

Jihad noted that T-bill interest rates have been lowered by “about 50 percent”. Cheaper loans from commercial banks will benefit the public and private sector, he said.

The MMA said in an announcement last month that the 28-day T-bill rate will be 3.50 percent (down from 7.50 percent), 91-day T-bill rate will be 3.87 percent (down from 8 percent), 182-day T-bill rate will be 4.23 percent (down from 8.50 percent), and 364-day T-bill rate will be 4.60 percent (down from 9 percent).

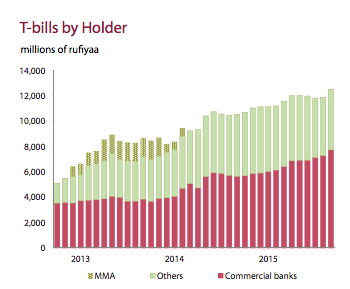

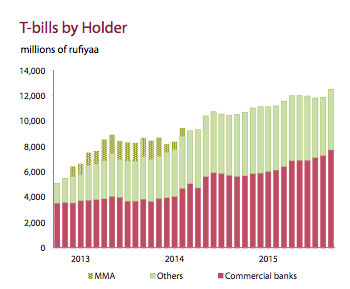

T-bills are short-term debt obligations that the government issues through the central bank to raise funds. The majority of T-bills are held by commercial banks.

The Maldives has been plugging shortfalls in revenue through the sale of T-bills. According to the Maldives Monetary Authority (MMA), the outstanding stock of government securities, including T-bills and T-bonds, reached MVR19.5 billion (US$1.2 billion) at the end of September.

The World Bank and the International Monetary Fund have said that high levels of public debt is the most pressing macroeconomic challenge facing the Maldives.

With government expenditure persistently outstripping income in recent years, public debt reached 75 percent of GDP or more than US$2 billion at the end of 2014.

Criticising the current administration’s “failed economic policies” in September, the main opposition Maldivian Democratic Party (MDP) had said that the budget deficit may increase four-fold if government spending is not reined in.

The government exceeded its budget deficit target of MVR1.3 billion (US$84 million) by the end of May, the MDP’s economic committee observed.

Despite record levels of income from taxes, the MDP said increased recurrent expenditure was forcing the government to rely on T-bill sales, resulting in reduced lending to the private sector as most of the T-bill debt is held by commercial banks.

In May, Jihad told The Maldives Independent that US$20 million grant aid obtained from Saudi Arabia for budget support will be used to “manage cash flow” as revenue was lower than expected.

Jihad said last night that efforts were underway to make the Maldives an “Islamic finance hub.”

The finance ministry and the MMA are also working together to strengthen the capital market authority, broaden the role of the Maldives stock exchange, and develop the bond market, he added.

A strong bond market will facilitate long-term financing for the government, Jihad said.

Discussion

No comments yet. Be the first to share your thoughts!

No comments yet. Be the first to join the conversation!

Join the Conversation

Sign in to share your thoughts under an alias and take part in the discussion. Independent journalism thrives on open, respectful debate — your voice matters.

Support Independent Journalism

Help us keep the news free and fearless

Give once

$

or

Become a memberfrom $5/month