Government’s estimate for 2015 economic growth unrealistic, says World Bank

High levels of public debt “driven by high and rising public spending” is the immediate macroeconomic challenge facing the Maldives, observed the World Bank’s South Asia Economic Focus report released last week. The government’s forecast for economic growth is 8.5 percent, but both the World Bank and the International Monetary Fund (IMF) expect the Maldivian economy to grow by 5 percent this year.

11 Oct 2015, 09:00

The government’s estimate for economic growth in 2015 is unrealistic with the performance of the tourism industry below expectations, says a World Bank report on South Asian economies.

The government’s forecast for economic growth is 8.5 percent, but both the World Bank and the International Monetary Fund (IMF) expect the Maldivian economy to grow by 5 percent this year.

High levels of public debt “driven by high and rising public spending” is the immediate macroeconomic challenge facing the Maldives, observed the World Bank’s South Asia Economic Focus report released last week.

With government expenditure persistently outstripping income in recent years, public debt reached 75 percent of GDP or more than US$2 billion at the end of 2014.

“Limited reserves, a high level of public debt and the short maturity of domestic debt adds additional vulnerability,” the report stated.

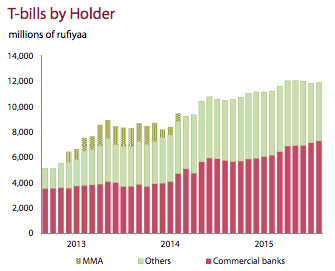

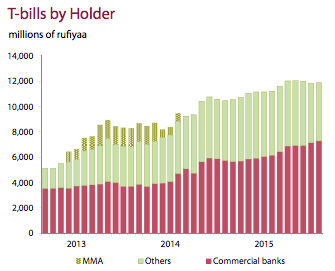

Shortfalls were plugged through the sale of treasury bills (T-bills), he said. According to the Maldives Monetary Authority (MMA), the outstanding stock of government securities, including T-bills and T-bonds, reached MVR18.9 billion (US$1.2 billion) at the end of August.

The central bank has meanwhile slashed interest rates on T-bills with effect from October 28.

The MMA said in an announcement last week that the 28-day T-bill rate will be 3.50 percent (down from 7.50 percent), 91-day T-bill rate will be 3.87 percent (down from 8 percent), 182-day T-bill rate will be 4.23 percent (down from 8.50 percent), and 364-day T-bill rate will be 4.60 percent (down from 9 percent).

Criticising the current administration’s “failed economic policies” last month, the main opposition Maldivian Democratic Party (MDP) had said that the budget deficit may increase four-fold if government spending is not reined in.

The government exceeded its budget deficit target of MVR1.3 billion (US$84 million) by the end of May, the MDP’s economic committee observed.

Despite record levels of income from taxes, the MDP said increased recurrent expenditure was forcing the government to rely on T-bill sales, resulting in reduced lending to the private sector as most of the T-bill debt is held by commercial banks.

Discussion

No comments yet. Be the first to share your thoughts!

No comments yet. Be the first to join the conversation!

Join the Conversation

Sign in to share your thoughts under an alias and take part in the discussion. Independent journalism thrives on open, respectful debate — your voice matters.

Support Independent Journalism

Help us keep the news free and fearless

Give once

$

or

Become a memberfrom $5/month